The stamp duty land tax (SDLT) treatment of purchases of mixed use property, such as a building with flats over commercial property, is complicated. Where there are a number of dwellings, calculations can be made of the SDLT liability with and without a claim to multiple dwellings relief to assess whether a claim for MDR should be made. This blog gives examples of how the calculations are carried out. It explains that for a mixed use transaction, when assessing the SDLT on the residential element, the higher rates do not apply (the extra 3% is not due).

UPDATE: This article was originally written on 22 August 2019, and updated on 27 April 2020. On 13 November 2020 HRMC updated their guidance at SDLTM09740 to state their view now is that the extra 3% will not apply to a transaction including dwellings and non-residential property where multiple dwellings relief is claimed.

They add a requirement that the non-residential element is neither negligible nor artificially contrived.

They say that they will shortly be updating the incorrect guidance at SDLTM29975. It was in a change to this guidance, almost exactly two years ago, where HMRC had first indicated that the higher rates (with the extra 3%) would apply to this kind of transaction. They will now say the higher rates will not apply.

It has taken a long time to get to this point!

Introduction

Does a claim to multiple dwellings relief trigger the higher rates for additional properties (HRAD or the 3% surcharge) where otherwise the mixed property rates would apply?

This article considers first a single transaction with dwellings and non-residential property, such as the purchase of a building with flats above shops, it concludes that the standard rates of SDLT apply in this scenario. It considers a test case HMRC brought which has now been decided on other grounds. The Appendix considers a more complex scenario with linked transactions.

Guidance

There was no published HMRC view on this question until the section in the Manual on Multiple Dwellings Relief was updated between 12 November and 9 December 2018.

The example at SDLTM29975 was updated to say that the higher rates would apply to the element of the price apportioned to the dwellings. The example in SDLTM29975 is of a single transaction (taking a long headlease) for £1.25M of a building comprising:

- 3 untenanted flats (£750,000)

- 2 flats subject to long leases (£100,000)

- 4 lock up shops (£400,000).

HMRC explain briefly how the calculation works with multiple dwellings relief and say the higher rates of SDLT will be applicable to the part of the price for the three untenanted flats.

HMRC do not in SDLTM29975 set out the tax calculation, but it would be as follows (assuming higher rates apply to the residential element):

SDLT on the £1.25M if MDR is not claimed is worked out at mixed rates (0%, 2% and 5%) and comes to £52,000.

With a claim to MDR the tax is worked out on two parts.

- For the consideration other than for the untenanted flats (£500K) the SDLT is 500K / 1,250K of £52,000 = £20,800.

- For the three untenanted flats (£750K) we take the average price of £250K. SDLT on that average price at surcharged rates (as assumed by HMRC) is £10,000, multiplied by three gives SDLT on the three of £30,000.

SDLT of £20,800 + £30,000 = £50,800, a modest saving against £52,000.

CALCULATION using standard rates

But the example appears to be wrong in assuming that for a single transaction the effect of claiming MDR is that higher rates apply to these dwellings.

If this assumption is wrong, the SDLT on the two flats subject to long leases and the four lock up shops stays at £20,800.

But the SDLT on the three untenanted flats would be worked out at standard rates on the average price of £250,000, so £2,500 multiplied by 3 to give SDLT on this element of £7,500 (at the minimum MDR rate of 1%).

£20,800 + £7,500 = £28,300. This is a £23,700 saving due to MDR.

WHY I have argued SDLTM29975 is wrong on this

- The higher rates of SDLT for dwellings can only ever apply to a “higher rates transaction” within the meaning of Finance Act 2003 Schedule 4ZA.

- Each of the charging provisions in para 3 to 7 apply only if the main subject of the transaction “consists of” a major interest in a single dwelling / in two or more dwellings.

- “Consists of” is different from the “consists of or includes” wording which can be found elsewhere in the SDLT legislation.

- So a transaction which includes non-residential property can never be a “higher rates transaction”.

- The wording in Sch4ZA/para2(2) is helpful, it provides that a transaction is a higher rates transaction if it falls within any of paragraphs 3 – 7 “otherwise it is not”.

- There is nothing in the way Finance Act 2003 Schedule 6B for MDR operates that turns it into a higher rates transaction.

- So when applying the rules to assess SDLT on the dwellings element of a mixed use transaction claiming MDR, the standard residential rates should apply, not the higher rates.

HMRC review of position

Contacts at HMRC confirmed that they see merit in this analysis of the interaction between HRAD and claims to Multiple Dwellings Relief on mixed residential/non-residential transaction: “namely that HRAD cannot form part of the MDR calculation in these circumstances”. HMRC said they were considering the point and would issue a more detailed response including a statutory analysis. It emerged that HMRC were delaying their more detailed response as they had a test case in process.

Details of the case were sparse, but it seemed to involve a property which, rather than actually comprising a number of dwellings and non-residential property, was bought with planning permission to build dwellings and a commercial element. So a preliminary issue would be whether MDR could apply where there was planning permission for dwellings, but no construction work had started.

Troy Homes as the test case

The decision in the combined appeal in the Troy Homes case was released on 1 April 2020. The case was decided in favour of the taxpayer on the basis that HMRC’s enquiry notices were not received by the taxpayer. As the notices had been sent to the companies’ registered office rather than to their principle place of business they were not deemed to have been served.

The Tribunal, being able to dispose of the two cases on this basis did not consider the substantive issues relating to multiple dwellings relief.

The decision gives very little detail of the transactions other than saying:

- Troy Homes (Inland) Ltd bought The Pheasant at Amersham on 26 May 2016 for £1,560,000.

- Troy Homes Ltd bought The Old Corn Barn at Roding on 19 April 2016 for £1,462,000.

Some research suggests that The Pheasant was a closed public house with planning permission for five new dwellings and the conversion of the old building to a sixth dwelling and a day care centre. The Old Corn Barn appears to have been commercial buildings with planning consent for demolition and the construction of six new dwellings.

What next?

HMRC said at the meeting of the SDLT Working Together Stakeholder Group on Thursday 23 April 2020 that as they no longer have a case in process, the Stamp Taxes Policy team is in the process of digesting the legal advice they have received on how MDR should apply a for mixed use where MDR is claimed. They say they will soon be issuing guidance.

Conclusion

The clarification we have been promised should help buyers correctly assess SDLT on mixed use cases, especially working out whether it is advantageous to claim multiple dwellings relief.

There must be cases where multiple dwellings relief has been claimed, but SDLT has been assessed at higher rates on the dwellings element, perhaps in reliance of the example in the Manual. It might be possible to claim back the overpayment here using overpayment relief. This relief can go back for four years; note though that the higher rates came into force on 1 April 2016, now over four years ago.

There might be other cases where it was considered not worth claiming MDR on the assumption that the higher rates would apply to the dwellings element. There is a time limit of 12 months from the “filing date” of the transaction to claim MDR by an amendment to a return. From 1 March 2019 the “filing date” was reduced to 14 days after the “effective date” of the transaction (normally completion). So calculations for mixed properties purchased within the last 12 months 14 days could be revisited to see if it saves SDLT to claim the relief.

See the Appendix for more complex calculations in a case involving a number of linked transactions, only one of which is mixed dwellings and non-residential.

Appendix

Worked example of five linked transactions:

Outline of transaction

A company acquired seven dwellings, two offices and agricultural land for £1.1M split into five transactions:

- Three flats for £360,000 and two offices for £150,000

- Agricultural land for £110,000

- One dwelling for £100,000

- One dwelling for £120,000

- Two dwellings for £260,000

Apportionment of price

- The amount paid for the dwellings was therefore £840,000.

- The remaining £260,000 was for the offices and agricultural land.

Three methods of calculating the SDLT

Method 1: No claim is made for MDR so SDLT on the total price is calculated on the Table B mixed property basis as some of the linked transactions include non-residential property. SDLT is worked out on slice rates with the top rate being 5%.

Method 2: A claim is made for MDR, so the residential elements are taxed at residential rates and the remaining consideration at a blended rate. This method uses the higher residential rates apply to all of the consideration for dwellings (this is for illustration only as it is believed this method is not correct for Transaction 1, the mixed use property).

Method 3: A claim is made for MDR, but this time on the basis that a single transaction with mixed property (Transaction 1) can never suffer the higher rates of SDLT.

Summary of amounts of SDLT

Method 1 (no claim to MDR) gives SDLT of £44,500.

Method 2 (MDR but using the method in the example in the HMRC Manual) gives SDLT of £35,718.

Method 3 (MDR but taking the view that the higher rates cannot apply to Transaction 1 as it is a mixed use transaction) gives SDLT of £28,518.

Calculations

METHOD 1 (no MDR)

This is “mixed use” property so work out the SDLT using Table B on £1,100,000. Method 1 does not involve a claim to Multiple Dwellings Relief.

The first £150,000 of the price has no SDLT, the next £100,000 has SDLT at 2% (£2,000) and the remaining £850,000 is subject to SDLT at 5% to give £42,500.

This comes to £44,500.

This total tax should be apportioned between the five transactions proportionately to the chargeable consideration for each.

METHOD 2 (with MDR)

SDLT is worked out claiming multiple dwellings relief on the method which HMRC set out in the Manual in the examples at SDLTMM29975 and SDLTM29977 which assume that the higher rates of SDLT (with the 3% surcharge) apply when MDR is claimed.

Total Price = £1,100,000

Total Dwellings Price = £840,000

Total Remaining Consideration = £260,000

In the calculations for Method 3 the full “step by step” calculation following the statutory provisions is set out. Similar detailed steps could be set out for Method 2 showing how the SDLT for each transaction is worked out, but it is relatively straightforward to work out the total SDLT over the linked transactions as set out in SDLTM29977:

- Because the average price of the 7 dwellings in the linked transactions is below £125,000, the SDLT on £840,000 is calculated at 3% to give £25,200.

- For the non-residential element we take an appropriate fraction of the SDLT which would have been due over the linked transactions absent the relief. This works out as 260,000 / 1,100,000 x £44,500 to give £10,518.

The sum of these two elements comes to £35,718.

METHOD 3 (with MDR but no higher rates on mixed use transaction)

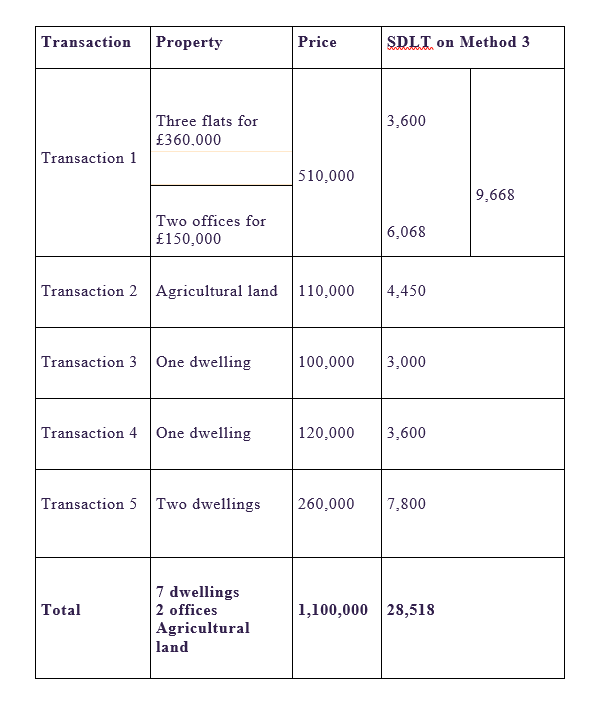

This method has been used to calculate the amounts of SDLT on the five transactions shown in the table below coming to a total of £28,518.

SDLT is worked out claiming multiple dwellings relief, but this time rejecting the method which HMRC set out in the Manual in the example at SDLTM29975 which assumes that the higher rates of SDLT (with the 3% surcharge) always apply when MDR is claimed. Instead the view is taken that Transaction 1 is itself a mixed use property and so is incapable of being a higher rates transaction within Finance Act 2003/Schedule 4ZA.

This method takes the view that under Finance Act 2003/section 55(1C), where transactions are linked, one has to work out the tax for each transaction on the basis of the rates of tax and the Table applicable to that relevant transaction, though allowing for linking using the method set out in s55(1C). On this view the first transaction cannot be a higher rates transaction and so the dwellings element has SDLT assessed on the “regular” Table A, not the surcharged Table A.

Transaction 1

FA03/Sch6B/para4(1) tells us to work out separately the tax on the consideration relating to the dwellings and the tax relating to the remaining consideration.

For the dwellings:

FA03/Sch6B/para 5(1) sets out four Steps which need to be applied for each transaction.

Step 1: Determine the amount of tax that would be due on the Total Dwellings Price under s55 if the property was entirely residential, but dividing the total price of the dwellings over the linked transactions by the number of dwellings in the linked transactions to give an average price. The average value over the linked transaction (£840,000 / 7) is £120,000.

It is at this point that the method varies from that in the Manual. This is on the basis that s55 calls on us to apply tax at the rates appropriate to the relevant transaction. The relevant transaction is mixed use and so is not a higher rates transaction. SDLT on the average value would be nil as the average value is under £125,000.

Step 2: Multiply by the number of dwellings. This would still give zero. But para 5(2) tells us to take 1% of the value, so that is £8,400.

Step 3: Ignore this step, as there are linked transactions.

Step 4: Multiply by the fraction CD (consideration for the dwellings for the relevant transaction) / TDC (total dwellings consideration).

This is 360,000 / 840,000.

This gives tax of £3,600 on the dwellings (1% of the value of the dwellings in Transaction 1).

For the remaining consideration:

Here we apply FA03/Sch6B/para5(7).

Tax on all the linked transactions without relief: £44,500.

We apply the fraction: Remaining Consideration / (Total Dwellings Consideration + Total Remaining Consideration). This is 150,000 / 1,100,000 giving tax of £6,068.

We add £3,600 to £6,068 to give £9,668 for Transaction 1.

Transaction 2

Here we apply FA03/Sch6B/para5(7).

Tax on all the linked transactions without relief: £44,500.

Fraction Remaining Consideration / (Total Dwellings Consideration + Total Remaining Consideration) is 110,000 / 1,100,000 giving tax of £4,450.

Transaction 3

Steps 1 and 2 of FA03/Sch6B/para 5(1) get us to £25,200 as the tax for all the dwellings in the linked transactions. Higher rates of SDLT are used as this transaction is for a dwelling only, so the 3% surcharge applies and SDLT comes out at 3% of 840,000 = £25,200.

We then take a fraction of it for the relevant transaction. The fraction is:

CD (consideration for the dwellings for the relevant transaction) / TDC (total dwellings consideration) is 100,000 / 840,000

This gives tax of £3,000.

Transaction 4

Steps 1 and 2 of FA03/Sch6B/para 5(1) get us to £25,200 as the tax for all the dwellings in the linked transactions. Higher rates of SDLT are used as this transaction is for a dwelling only, so the 3% surcharge applies and SDLT comes out at 3%.

We then take a fraction of it for the relevant transaction. The fraction is:

CD (consideration for the dwellings for the relevant transaction) / TDC (total dwellings consideration) is 120,000 / 840,000.

This gives tax of £3,600.

Transaction 5

Steps 1 and 2 of FA03/Sch6B/para 5(1) get us to £25,200 as the tax for all the dwellings in the linked transactions. Higher rates of SDLT are used as this transaction is for dwellings only, so the 3% surcharge applies and SDLT comes out at 3%.

We then take a fraction of it for the relevant transaction. The fraction is:

CD (consideration for the dwellings for the relevant transaction) / TDC (total dwellings consideration) is 260,000 / 840,000.

This gives tax of £7,800.

For professional advice on SDLT please contact Blake Morgan’s SDLT expert, John Shallcross.

This article is intended for general information purposes only and does not constitute legal or professional advice. Advice should be sought before proceeding with any transaction.

This article was originally posted by John Shallcross on 22 August 2019, and last updated on 27 April 2020.

Explore more insights

Articles

Articles 12 May

Upwards-only rent reviews: what the new statutory ban means for commercial leases

The long‑anticipated ban on upwards‑only rent reviews (UORRs) has now been enacted as part of the English Devolution…

Articles

Articles 08 April

The Renters’ Rights Act 2025: five things to do before 1 May 2026

With Phase 1 of the Renters’ Rights Act 2025 taking effect on 1 May 2026, what do landlords…

Articles

Articles 26 March

Key risks for tenants across the life of a commercial lease

What are the risks for commercial tenants and how can you mitigate them? Our Property Dispute Resolution team…