Businesses must now do more to provide information to individual debtors and attempt to settle before taking them to court.

The new Pre-Action Protocol for Debt Claims (PAPDC) comes into force on 1 October 2017, and applies to any claim by a business (including individual sole traders and public bodies) (the creditor) for a debt owed by an individual (also including a sole trader) (the individual).

The PAPDC does not apply where the creditor is not a business, or where the debtor is a business other than a sole trader.

The PAPDC builds on the existing requirements of the Practice Direction on Pre-Action Conduct, but it goes further with more detailed requirements and longer timescales for exchanging information.

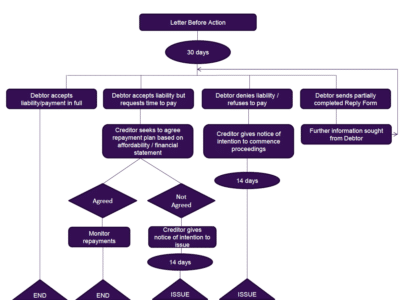

Under the PAPDC, the creditor must send a detailed Letter of Claim setting out certain mandatory information, including details of the amount of the debt, how the debt arose, and details of any interest being claimed.

The creditor is required to wait at least 30 days after sending the Letter of Claim before taking the matter to court, and may be expected to allow additional periods if the individual requests information or documents, or indicates that they are seeking advice, or wishes to negotiate a payment plan.

The individual must be given a Reply Form with the Letter of Claim, in which they should explain whether they admit or dispute the debt, or indicate that they are seeking legal or debt advice. If they dispute the debt then they should explain their reasons, and if they admit the debt then they should provide detailed financial information and propose an affordable payment arrangement, e.g. an instalment plan.

The parties should attempt to agree an affordable payment plan if possible. This does not affect any liability the individual may have to settle the debt immediately, but creditors should be aware that even if they take the matter to court and obtain judgment, the court can order an instalment plan anyway if the individual is of limited means.

If the debt is disputed, the parties should discuss the matter and exchange relevant information/documents and attempt to reach agreement, making use of ADR where appropriate.

Where liability and/or repayment terms cannot be agreed, the creditor may give notice to the individual that they are taking the matter to court.

If the parties agree a repayment plan, but the individual then breaches it and the creditor wishes to take them to court, the creditor must comply with the PAPDC afresh. Repayment plans should be made conditional on full compliance by the individual. Otherwise, the creditor may only be able to claim for overdue instalments under the new payment plan, causing additional delay.

Compliance with the PAPDC is mandatory. Failure to comply will not prevent court proceedings being issued, but the Court may decide to stay the claim to allow time for compliance, or penalise the defaulting party, e.g. by ordering them to pay costs.

Given the new extended processes that need to be followed (and which may even need to be re-started in some instances), it is important for businesses to ensure that credit control and pre-court processes are run as efficiently as possible to reduce unnecessary delays when seeking payment of debts from individuals. Creditors should err on the side of providing more complete information and relevant documentation when first writing the Letter of Claim, as it may cause delays if they are asked to provide it later.

It is important to remember that the PAPDC only applies to debts owed by an individual to a business. Cases where the creditor is an individual, (other than a sole trader) or the debtor is a business (other than a sole trader), are unaffected.

Speak to a member of our Insolvency & Business Support team

Arrange a callHow can we help?

To get in touch with one of our legal experts please fill in your details.

Explore more insights

Articles

Articles 12 May

UKIPO: 150 years of trade marks

The UKIPO has celebrated 150 years of trade marks this year. To mark the occasion, we look at…

Articles

Articles 30 April

Finance Act 2026: key updates to EMI and EOTs

The Finance Act 2026 received royal assent on 18 March 2026 and introduced favourable reforms to EMI rules…

Articles

Articles 28 April

CMA imposes £4.2m penalty and orders refunds in AA/BSM drip pricing enforcement action

If you are a business supplying goods or services to consumers in the UK, you need to take…