Last week experts from Blake Morgan and Griffins discussed the recently published Corporate Insolvency and Governance Bill, and how items such as suspending wrongful trading obligations will impact directors’ duties and businesses whilst they are trying to manage the current situation.

We had over 140 attendees join us for the webinar, ask questions to the panel and listen to their discussion. Thank you to everyone who joined us, for the questions we couldn’t answer live, here is a selection we’ve put to our panel after the event.

If you have any further questions, please get in touch.

Q&A

Despite the protection measure, if a director is found to have not acted within their fiduciary duties will they still remain at risk of disqualification and in addition potentially personally liable to make a payment to the Insolvency Service?

Stephen – Absent of any legislation to the contrary then I would imagine that the risk remains. It could be that the Disqual Unit are issued with a directive not to pursue directors for this period and it is possible that Judge’s exercise their discretion more freely because of the virus, but the risk remains.

Katie – I agree entirely with Steve. I have not seen any amendments to the Company Directors Disqualification Act 1986 and am not aware of any directives to the Disqual Unit. Many directors are disqualified for trading to the detriment of the Crown, which I think is the key risk here. At present, HMRC has granted significant forbearance to companies, but it is not clear whether in circumstances where directors have availed themselves of that forbearance and have continued to pay themselves, landlords, other suppliers and so are technically trading to the detriment of the Crown, how the Courts will consider that. It would seem particularly unfair for a director to be disqualified in these circumstances, without something more and it would arguably be against the Government’s policy to encourage companies to continue trading. However, the risk is still there.

The current climate seems to have created a lock up in working capital flow. How should companies go about prioritising payments as working capital lock up drips through, whilst not falling foul of creating a preference where a risk of cash-flow insolvency looms?

Stephen – As I answered in the webinar, short term payments will be viewed with hindsight in the longer term, so in making short term payments the director needs to have a clear idea of what the long term strategy is and is it assisted by these payments.

Katie – The key is understanding what is crucial to the business i.e. what payments if they are not made will stop the business from trading. This may depend on the attitude of individual creditors – some may not be willing to deliver without cash on delivery. Effective directors will understand the cash flow of the business on a short term, medium term and longer term basis and be able to make decisions on that basis. Those cash flows will need to be reviewed regularly on a worst case, medium case and best case scenario.

Not really a question. Does the panel think this legislation is just to kick the can down the road?

Trevor – I see it as a bridge until the roads get reopened.

Katie – As with many things, it will depend on how it is used. If the statutory moratorium simply becomes a precursor to administration or liquidation, then yes it is hard to see it as anything other than a tool for kicking the can down the road. If however, companies are able to recover within the breathing space afforded by the statutory moratorium and return to solvency, then it will achieve its aim.

While the directors may not have to contribute personally due to a new act for decisions taking during the relevant period, would they still be guilty of wrongful trading with all implications that come with that, especially possibility of being a director going forward?

Stephen – Our criticism of the proposed legislation is that it is hard to say. As the purpose of the legislation is to reassure directors that is clearly a problem.

Katie – Because of the many tools available to officeholders, it is difficult to say that the wrongful trading provisions in the Bill (Corporate Insolvency and Governance Bill) mean that a director won’t have to face liability at all. For example, a director could still be at risk of misfeasance, perhaps by allowing the company to grant preferences or transactions at undervalue.

Katie, you mentioned the monitor can be challenged by creditors. Surely without the ability of the monitor to challenge the directors, the monitor is exposed to a level of risk in that they have to rely solely on the information delivered up to them by directors potentially facing major financial distress. Can the monitor cease to act if they are not convinced as to the validity of the information given to them?

Katie – Yes, the monitor is entitled to terminate the statutory moratorium if the directors are not giving the monitor sufficient information. However, going to Court to get that information is costly. It is easy to see a situation in which the monitor’s costs are challenged by creditors, but those costs may have been increased because of the lack of co-operation from the directors. I think secured lenders will be particularly concerned because the costs of the moratorium have super priority in any subsequent insolvency and this might be priced into lending going forward.

Stephen – Their power seems to be to end the moratorium or apply to court if uncertain. The monitor can of course demand more information but then the costs increase and the monitor is in danger of their role changing if they are too proactive.

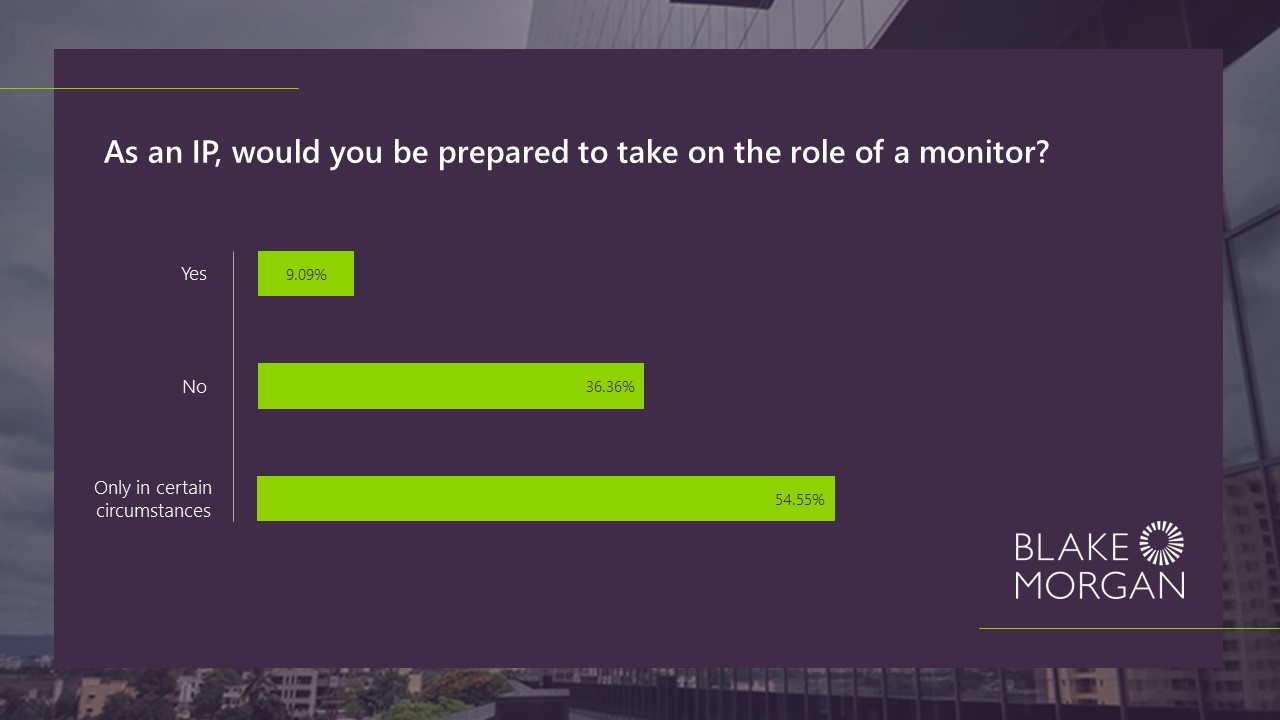

Data from the poll

We ran a live poll during the webinar, asking whether an insolvency practitioner (IP) is prepared to take on the role as a monitor. You can see the answers below and view a recording of the webinar here.

Much of the information surrounding the safeguarding against winding up orders seems to be focused towards commercial tenants. Are there any restrictions on the type of creditor which the legislation will apply to regarding winding up petitions?

Stephen – None that I am aware of.

Katie – No, the Bill (Corporate Insolvency and Governance Bill) does not specify any restrictions against particular creditors. It applies to all creditors.

What is the best course of action for a creditor where the customer could not pay its debts prior to COVID-19 and now believes it can hide behind the cloak of COVID-19 and this new legislation?

Katie – It is possible to present a winding up petition, but the creditor must be able to show that the debtor’s financial problems are not COVID-19 related. Without internal information, such as management accounts, that will be difficult. There are no restrictions on the use of county court judgments, charging orders, third party debt orders or orders to obtain information from judgment debtors under the Civil Procedure Rules. However, the creditor may be throwing good money after bad going down this route too.

Stephen – That will change with time but subject to specific legal advice the main tactic from creditors in that situation is to monitor the position and seek further explanation from the debtor.

Given the Tsunami of insolvencies anticipated do you think that there will be enough IPs around to deal with expected workloads? Is this new toy likely to add to confusion amongst creditors (and the press and public) who already understand insolvency (very) poorly.

Stephen – I think there is a danger in treating as fact that there will be a tsunami as the government’s policies are very much aimed at that not happening and further measures may be taken. As with previous recessions, staff from many firms will come from the audit and other teams although it is possible that there are fewer multi-discipline practices than in previous crashes.

As for the new toy, again we have had them before. Some have been enthusiastically taken up by the profession and others have been given as sniff and then never spoken about again. I am confident that the profession will find the cracks quickly.

Katie – The profession went through significant changes between 2008 and 2012, and from my own experience in the legal side of things, there is a dearth of experienced insolvency lawyers. That said, I think the profession is very used to adapting and see no reason why it will not do so again.

I anticipate some frustration from creditors with the statutory moratorium, particularly if rescue is not possible and another insolvency procedure follows. In an extended statutory moratorium those creditors could be out of pocket for at least a year. With HMRC becoming a preferential creditor for VAT, PAYE and employees NIC in December 2020, creditors may feel like they are getting an ever decreasing share of the shrinking pie. Much will depend on how the statutory moratorium is used.

Most of the directors I’m talking to who are blaming C19 (COVID-19) for their issues were insolvent three years ago, slightly worse, two years ago, still worse one year ago. C19 isn’t their problem – they have broken the first law of holes – when in one, stop digging.

Trevor – For businesses that ended their financial years in the months just prior to CV (COVID-19), there are statistical tools that can show whether a business is in distress or not. If it is likely that a business was already distress before CV, then the monitor or the court may refuse appointments / moratoriums

Stephen – I recommend Trevor Slack’s articles on Z Scores for exploring this!

Katie – The theory is that the changes should not be a free pass for directors whose companies have been insolvent for some time, and not as a result of COVID-19. However, the reality is that it is difficult to legislate perfectly on this issue, particularly given the speed at which the Government has moved on this. That said, I think insolvency practitioners and the Courts are used to separating those directors who are entitled to help and those that aren’t.

Isn’t the duty simply to take every step possible to minimise losses to creditors?

Trevor – If a business caught out by CV can trade back to profitability, if given interim support, then that should minimise losses to creditors. But if it is questionable that a business can do so, e.g. because it had problems prior to CV, or CV has made it nonviable regardless, then it should probably be wound up.

Stephen – My point about the lack of a duty to liquidate is simply that I cannot find it neatly articulated in legislation or case law. It makes sense for a loss-making business to cease trading and it makes sense for a business that has ceased to trade to wind up its affairs and distribute its assets. I just couldn’t readily lay my hands on the principle, but it is around somewhere.

Katie – Section 214 (3) states: “The court shall not make a declaration under this section with respect to any person if it is satisfied that after the condition specified in subsection (2)(b) was first satisfied in relation to him that person took every step with a view to minimising the potential loss to the company’s creditors as he ought to have taken.” So as soon as a director realises, or should have realised, that the company has no reasonable prospect of avoiding insolvency liquidation, then they should take every step with a view to minimising the potential loss. If they cannot do that, then they should cease trading and/or look to liquidate the company.

It doesn’t mean run into the arms of a liquidator – that may be rats/ships…

Katie – It could also be argued that by liquidating a company too early that the directors have breached their duties to the company and/or the creditors. It all comes back to understanding the company’s cash flows and business plans and the impact that any rescue is likely to have, and making decisions accordingly.

Yes – it is rebuttable – but you have to take “every step” and I’m sure we could all come up with other/additional steps that could/should have been considered…

Stephen – ‘Every step’ has been explored a little in case law but I get the sense that it is intended to be a very high test but not an impossible one. I believe that a court could find that the director taking proper reasonable steps has met this test. As this defence only applies to directors who have concluded insolvent liquidation is unavoidable then I imagine that a majority of the steps are fairly standard.

Katie – Steve is right in that before you get to “every step”, the Court must be satisfied that the director knew or ought to have known that the company had no reasonable prospect of avoiding insolvent liquidation. The director is assessed against a reasonably diligent person having both the general knowledge, skill and experience that may reasonably be expected of a person carrying out the same functions as are carried out by that director, as well as the general knowledge, skill and experience that that director has. Only once the Court has found that the director knew or ought to have known that the company has no reasonable prospects of avoiding insolvency liquidation, does it then assess whether “every step” has been taken.

Dishonesty is not required, but it is quite difficult to prove or disprove someone else’s knowledge, particularly when you are dealing with a small company which operates in an informal manner; evidence of creditor pressure, late filing of accounts, insolvency on a balance sheet basis, only paying creditors when proceedings or statutory demands have been issued will assist. In Re DKG Contractors Ltd [1990] B.C.C. 903, it was held that, as soon as the directors knew that a creditor had refused further supplies because of lack of payment and that other creditors were pressing, they should have introduced some financial controls, which would have shown the inevitability of insolvent liquidation. The directors were therefore liable for wrongful trading from that time. The fact that their own knowledge, skill and experience was “hopelessly inadequate” did not protect them.

I am hopeful that the proposal is mostly about stopping those IPs who like to scare directors into their arms from being so easily able to do that.

Stephen – As Des Flynn once said, we do not legislate on the assumption that licensed IPs will act improperly.

Katie – I think that there are situations where administration is the proper course of action, but where the value of the business and/or assets cannot justify the costs. I would hope that the new statutory moratorium would help in these situations.

How can you make a supplier supply?

Stephen – Legal advice and the threat of enforcement.

Katie – If a supplier ceases to supply a company because of the company’s insolvency, that will be a breach of contract. The company via its officeholder can bring a claim against that supplier for breach of contract and damages, and/or an order for specific performance, by which the supplier is compelled to continue the supply. I see no reason why normal costs rules would not apply so that if such proceedings were necessary, the supplier would also likely have to pay the costs of the company and its officeholder in bringing those proceedings. I would hope that an appropriately worded letter would persuade a supplier to continue to supply.

Speak to a member of our Insolvency & Business Support team

Arrange a callHow can we help?

To get in touch with one of our legal experts please fill in your details.

Explore more insights

Articles

Articles 15 July

AIM reimagined: how the 2026 AIM consultations could help reshape the market

AIM’s June 2026 consultation by the London Stock Exchange (LSE) is more than a technical tidy up. We…

Articles

Articles 15 July

When the computer says no: AI and ‘meaningful human involvement’ in recruitment

Care is needed by employers using AI in recruitment. What do data controllers need to do, what constitutes…

Articles

Articles 01 July

ECCTA 2023: company directors and IDV… where are we now?

What is the objective of the Economic Crime and Corporate Transparency Act (ECCTA) 2023 with regards to identity…